Ireland: Domicile of Choice for Private Funds

Ireland has updated and modernised its regulatory framework governing investment limited partnerships (ILPs). Our Investment Funds team explores how the enhancements to the ILP regime can help Ireland compete with limited partnerships in other leading jurisdictions. Ireland has updated and modernised its regulatory framework governing investment limited partnerships with the passing of the Investment Limited Partnership (Amendment) Act 2020 (ILP Act). The ILP Act is designed to meet the needs of investment funds and their investors. The enhancements introduced by the ILP Act means that Ireland can compete with limited partnerships in other leading jurisdictions. This is making Ireland a domicile of choice for the establishment of private funds in the following categories:

- Private equity

- Real estate

- Infrastructure, and

- Sustainable investment

We explain the key features of the ILP legislation which will be of interest to asset managers and promoters of private funds.

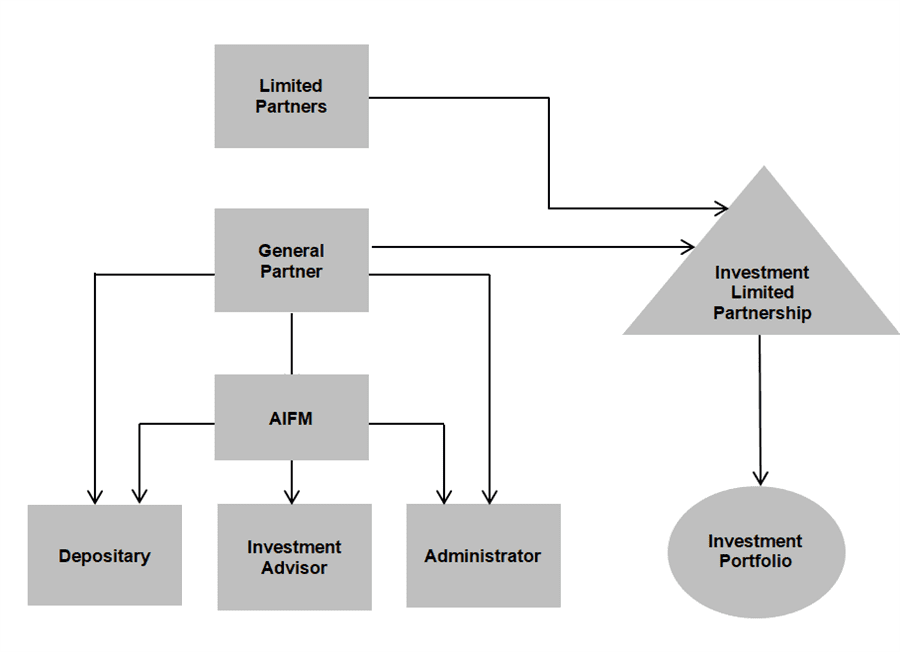

What is an investment limited partnership?

An Investment Limited Partnership is both a common law partnership and a regulated investment fund that is authorised by the Central Bank of Ireland (Central Bank). As a common law partnership, an ILP is constituted under a limited partnership agreement that is entered into by at least one general partner (GP) and one or more limited partners (LP). The rights and obligations of the GP and LPs are set out in:

- The limited partnership agreement

- The ILP Act, and

- Common law principles governing the operation of partnerships

The ILP is also subject to regulation under the Central Bank’s Alternative Investment Fund (AIF) Rulebook.

The principal business of an ILP, as set out in the limited partnership agreement, is the investment of its funds in all kinds of property or securities. An investment limited partnership is not a separate legal entity; however, the general partner represents the ILP and usually enters into contracts on its behalf.

Regulatory regimes

An ILP may be established as a retail fund, which we refer to as a Retail Alternative Investment Fund (RIAIF). Alternatively, it is also referred to as a fund that is restricted to qualifying investors which is known as a Qualifying Investor Alternative Investment Fund (QIAIF). In each case, the ILP will be regulated by the Central Bank and it is required to comply with the provisions of the Central Bank’s AIF Rulebook. In addition, according to the Alternative Investment Fund Managers Directive (AIFMD), the GP is required to appoint an Alternative Investment Fund Manager (AIFM) who is responsible for the management of the ILP.

Structure Chart

Modernisation of ILP legislation

The ILP Act has reformed the regime for investment limited partnerships and introduced the following key enhancements:

- Umbrella structure: An investment limited partnership may be established as an umbrella collective investment vehicle with multiple sub-funds. Under the ILP Act each sub-fund has segregated liability. Therefore, the assets of one sub-fund may not be used to discharge the liabilities of another sub-fund within the umbrella ILP structure. The ability to utilise an umbrella partnership vehicle allows sponsors to bring funds to market quickly by utilising existing contracts and service providers for subsequent funds.

- Investor liability: Under Irish partnership law, a limited partner may be liable for the debts of the partnership if it participates in the management of the partnership. The ILP Act extends the list of safe harbour provisions. It also provides examples of the types of activities that an LP may carry out without being considered as taking part in the management of the ILP, thereby preserving the LP’s limited liability status. These include participating in advisory committees and voting on strategic matters affecting the business of the ILP.

- Distributions and liability of LPs: The ILP Act clarifies that a partnership may distribute and return capital to limited partners if the investment limited partnership is solvent at the time the distribution is made. In addition, the ILP Act clarifies that an LP shall not in any circumstances be liable for the debts or obligations of the ILP beyond the capital contributed by the LP.

- LP default protections: The ILP Act provides that if an LP fails to perform its obligations or breaches the limited partnership agreement, the sanctions a general partner may impose on the defaulting LP will not be unenforceable under Irish law. This is because they are penal in nature. This provision protects the enforcement measures that a GP may take against a defaulting LP in the best interests of LPs as a whole.

- Amendments to the LPA: The ILP Act aligns the investment limited partnership with other Irish fund structures by removing the requirement for the unanimous consent of LPs regarding an amendment of the LPA. Under the ILP Act, an LPA can be amended by:

- approval of a majority of LPs provided the LPA allows for changes via majority, or

- with the consent of the depository who is required to certify that the changes to the LPA do not prejudice the interests of the LPs.

- Migration: The ILP Act provides a statutory process to facilitate migration of limited partnerships established in other jurisdictions to Ireland by way of continuation. The application for migration by a migrating partnership is made to the Central Bank. The application follows much of the standard process for establishment and authorisation of an investment limited partnership.

- Replacement of GP: The replacement of a general partner is facilitated under the ILP Act. This is done by confirming that property rights of every type held by a departing GP will automatically vest in the incoming GP without formalities or notification being required. The property rights include “all choses in action” and rights to make capital calls and receive the proceeds.

Key benefits of an investment limited partnership

- Regulatory status: The investment limited partnership is regulated and subject to the prudential supervision of the Central Bank. As a regulated fund established in an OECD onshore jurisdiction, an ILP should be a suitable vehicle for raising capital from institutional investors who are often restricted on the extent to which they can invest in unregulated vehicles or offshore vehicles.

- Capital raising: A investment limited partnership that is managed by an authorised alternative investment fund manager in the EU can avail of the marketing passport under Alternative Investment Fund Managers Directive and may be marketed to professional investors throughout the EEA.

- Flexible fund product: A investment limited partnership authorised as a Qualifying Investor Alternative Investment Fund (QIAIF) is not subject to material investment restrictions. Also, the type of assets an ILP may hold is not restricted. Accordingly, ILPs may be established as, for example, real estate funds, private equity funds or infrastructure funds.

- Speed to market: A investment limited partnership designated as a QIAIF is subject to a fast track authorisation procedure and may be authorised by the Central Bank within 24 hours of receipt of the application.

- Tax status: A Investment Limited Partnership is tax transparent meaning that the partnership itself is not subject to tax on its income or gains. Consequently, there should be no tax leakage in using an ILP. The limited partners will be subject to tax under the tax code of their country of residence and the country where the investment is situated. This is subject to any relief available under a double tax treaty between the country of residence of the LPs and the country where the investment is situated.

- Ireland as a centre of excellence: Ireland is the largest fund administration centre in the world with more than €5.4 trillion assets under administration. There is currently over €3.9 trillion in fund assets domiciled in Ireland. Ireland’s attraction as a fund domicile is based on the combination of the Irish legal and regulatory system, the specialist skills and expertise of its workforce, the country’s pro-business approach, infrastructure, competitive tax environment and government support.

The modernised Investment Limited Partnership puts Ireland firmly on the map as a domicile of choice for asset managers seeking to establish private funds within a regulated ILP framework. The ILP, coupled with the benefits of utilising the AIFMD passport to raise capital from EU professional investors, makes Ireland an ideal location for establishing private funds. We have advised extensively on the establishment of partnerships and other private investment vehicles. As a full service Irish law firm, we have the strength and depth in relevant practice areas including investment funds, tax, banking, corporate and real estate that enables us to advise on the most complex fund structures.

If you would like to discuss any related queries, please contact a member of our Investment Funds team.

The content of this article is provided for information purposes only and does not constitute legal or other advice.

Common questions

What is an investment limited partnership? An Investment Limited Partnership is both a common law partnership established under the Investment Limited Partnerships Act 1994 (as amended) and a regulated investment fund that is authorised by the Central Bank of Ireland. |

What is a limited partnership in Ireland? A limited partnership is a common law partnership established under the Limited Partnerships Act 1907 (as amended) and unlike the Investment Limited Partnership does not require Central Bank of Ireland authorisation or regulation. Accordingly, 1907 limited partnerships are unregulated. |

Can a limited partnership be an investment company? No, a limited partnership cannot be an investment company because as a common law partnership it does not have separate legal personality unlike an investment company which does. |

Why domicile a fund in Ireland? Ireland’s attraction as a fund domicile is based on the combination of the Irish legal and regulatory system, the specialist skills and expertise of its workforce, the country’s pro-business approach, infrastructure, competitive tax environment and government support. |

How many funds are domiciled in Ireland? As at November 2022, there were 8,693 funds including sub-funds domiciled in Ireland. |

Share this:

Related Content

-

Insights Financial Services

-

Insights Financial Services

-

Insights Technology

-

Events Financial Services

-

Insights Financial Services

-

News Financial Services

-

News Built Environment

-

News Financial Services

-

Insights Financial Services

-

News Financial Services