The European Commission has now formally adopted the European Sustainability Reporting Standards. This brings much-awaited clarity on the detailed reporting requirements which will apply under the EU’s new Corporate Sustainability Reporting Directive. Emer Shelly, Partner, Corporate Governance, takes a look at this latest development.

A significant milestone has been reached on the path towards the implementation of the EU’s new corporate sustainability reporting framework.

The European Commission recently formally adopted the first set of common sustainability reporting standards, known as the European Sustainability Reporting Standards (ESRS). Once implemented in Irish law, they will bring long-awaited clarity, particularly to large undertakings in the EU, on the extent of impending sustainability reporting obligations under the Corporate Sustainability Reporting Directive (CSRD). Read our previous articles on the CSRD on our ESG Hub.

Purpose and overview of the ESRS

The demand for sustainability information continues to grow exponentially, primarily driven by investors who are increasingly conscious of the risks and opportunities that environmental, social and governance issues pose for organisations. However, the lack of consistency to date in how organisations choose to report on sustainability matters has created significant challenges. These include investors and other stakeholders being hindered from effectively comparing and benchmarking sustainability information, and making it difficult to identify instances of greenwashing.

The CSRD aims to increase stakeholder access to relevant, reliable and comparable sustainability information. It therefore empowered the European Commission to develop and adopt the ESRS, a mandatory set of common reporting standards. These reporting standards set out in prescriptive detail the nature of the information that must be disclosed and how the information must be disclosed.

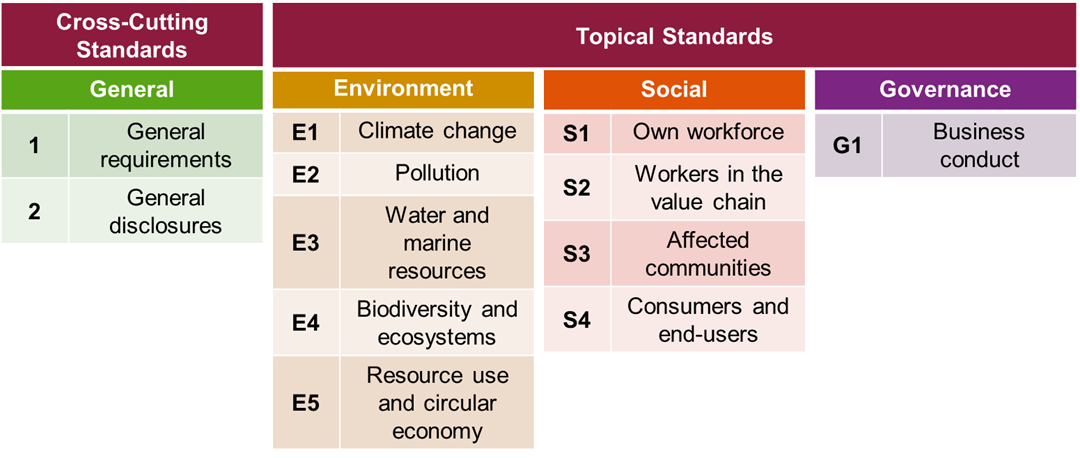

The first set of ESRS were developed by the European Commission in consultation with the European Financial Reporting Advisory Group (EFRAG) following extensive stakeholder engagement and public consultation processes. They have now been formally adopted by the European Commission by way of delegated act. They comprise 12 standards as follows:

Key changes from earlier draft ESRS

The final ESRS differ in a number of ways from the earlier drafts which were prepared and submitted to the European Commission by EFRAG in November 2022.

Additional flexibility for assessing materiality

- The final form ESRS prescribe that the general “cross-cutting” disclosure requirements set out in ESRS 2 and which apply across all sustainability topics are mandatory for all organisations. However, the disclosure requirements set out in all topical Environment, Social and Governance standards will apply only to the extent they are deemed to be material to an organisation following a robust materiality assessment.

- This means that, contrary to EFRAG’s proposals, disclosures in relation to climate change (ESRS E1) and certain disclosures regarding an organisation’s own workforce (ESRS S1) are no longer always mandatory. Instead, those topics will be subject to the same materiality assessment as all other sustainability topics in the topical standards. However, any organisation that concludes that climate change is not a material topic and does not report on it must explain its conclusion in detail in its report.

Increased transitional arrangements

- The final form ESRS introduce some additional phase-in provisions to provide scope to organisations with less than 750 employees to omit certain disclosure requirements during the first year, or in some cases two years, of its sustainability reporting. The concessions apply to disclosure requirements under certain environmental standards, including on scope 3 emissions (ESRS E1) and biodiversity (ESRS E4), and to all disclosure requirements under the social standards (ESRS S1-S4).

More voluntary reporting requirements

- The final form ESRS contain a slightly increased number of voluntary disclosures than that proposed by EFRAG in order to reduce the burden for organisations of complying with certain more costly and challenging disclosure requirements.

The changes introduced by the European Commission have been criticised by many who claim they give rise to increased complexity, create the potential for inconsistency in reporting and weaken the overall ambition of the ESRS. However, for many organisations facing the onerous task of collecting and reporting extensive data, particularly those doing it for the first time, the additional breathing room will no doubt be very welcome.

It is also worth noting that additional ESRS are expected to be adopted in due course, including industry-focused sector-specific standards, more limited and proportionate standards for listed SMEs and standards which are specific to in-scope non-EU companies.

Further CSRD updates

Member States have until July 2024 to transpose the CSRD into their national law. In Ireland, the preparation of the draft transposing regulations is well underway. The Department of Enterprise, Trade and Employment (DETE) has confirmed that they expect them to be finalised by the end of this year.

Conclusion

The adoption of the ESRS marks a significant milestone in the EU's journey towards a more sustainable and transparent business landscape. With the formal adoption of the first set of ESRS, organisations within the scope of the CSRD can now set a clear path to prepare for their sustainability reporting obligations.

For more information on or to discuss how the CSRD may impact your business, contact a member of our Corporate Governance team or visit our ESG hub.

The content of this article is provided for information purposes only and does not constitute legal or other advice.

Share this:

Related Content

-

Insights Corporate Governance

-

Insights Corporate

-

News FIRMWIDE

-

Insights Corporate Governance

-

News Artificial Intelligence (AI)

-

News FIRMWIDE

-

Insights FIRMWIDE

-

News Life Sciences

-

Insights Life Sciences

-

Insights Competition, Antitrust & Foreign Investment

-

Insights Corporate Governance

-

Insights Corporate

-

News FIRMWIDE

-

Insights Corporate Governance

-

News Artificial Intelligence (AI)

-

News FIRMWIDE

-

Insights FIRMWIDE

-

News Life Sciences

-

Insights Life Sciences

-

Insights Competition, Antitrust & Foreign Investment

-

Insights Corporate Governance

-

Insights Corporate